Checking Vs Savings Account

adminse

Apr 03, 2025 · 7 min read

Table of Contents

Checking vs. Savings Accounts: Unlocking Financial Freedom Through Understanding Your Options

What makes understanding checking and savings accounts crucial for financial well-being?

Mastering the nuances of checking and savings accounts is the cornerstone of sound financial management, paving the way for a secure and prosperous future.

Editor’s Note: This comprehensive guide to checking vs. savings accounts has been published today to provide readers with up-to-date information and actionable strategies for managing their finances effectively.

Why Understanding Checking and Savings Accounts Matters

The distinction between checking and savings accounts might seem straightforward, but a deep understanding of their unique features and functionalities is vital for individuals at all stages of their financial journeys. These accounts form the bedrock of personal finance, impacting everything from daily transactions to long-term savings goals. Choosing the right account for your needs can significantly impact your financial health, helping you avoid unnecessary fees, maximize interest earnings, and streamline your financial management. Ignoring these differences can lead to missed opportunities and potential financial setbacks.

Overview of the Article

This article delves into the core differences between checking and savings accounts, exploring their features, benefits, drawbacks, and ideal applications. We will examine various account types within each category, highlighting the factors to consider when choosing an account that aligns with individual financial objectives. Readers will gain actionable insights and a clear understanding of how to leverage these accounts to achieve their financial goals.

Research and Effort Behind the Insights

This article is the result of extensive research, incorporating information from reputable financial institutions, consumer advocacy groups, and relevant government regulations. We’ve analyzed numerous account offerings from various banks and credit unions to provide a comprehensive and unbiased comparison. Data points on interest rates, fee structures, and account features are drawn from publicly available information and industry benchmarks.

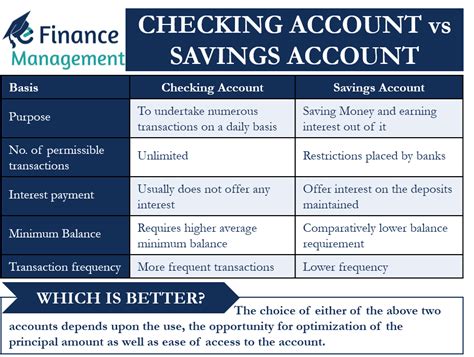

Key Differences: Checking vs. Savings Accounts

| Feature | Checking Account | Savings Account |

|---|---|---|

| Primary Use | Daily transactions, bill payments, debit purchases | Saving money, earning interest |

| Access | Easy access, unlimited transactions | Limited transactions, potential restrictions |

| Interest Rate | Typically low or nonexistent | Generally higher than checking accounts |

| Fees | Monthly maintenance fees, overdraft fees possible | Monthly maintenance fees possible, low balance fees |

| Checks | Checks readily available | Checks typically not available or limited |

| Debit Card | Usually included | May or may not be included |

Smooth Transition to Core Discussion

Let’s now delve deeper into the specific characteristics of checking and savings accounts, exploring their practical applications and helping you determine which account, or combination of accounts, best suits your individual needs.

Exploring the Key Aspects of Checking and Savings Accounts

1. Transactional Capabilities: Checking accounts are designed for frequent transactions. They offer debit cards for purchases, ATM access for cash withdrawals, and the ability to write checks for payments. Savings accounts, conversely, prioritize saving money, and usually have transaction limitations to encourage consistent saving. Frequent withdrawals might incur fees.

2. Interest Rates and Earnings: Savings accounts generally offer a higher interest rate than checking accounts. While the interest might be modest, it serves as a crucial component of long-term savings growth. Checking accounts rarely offer significant interest, focusing instead on facilitating transactions. The choice between higher interest and ease of access is a key consideration.

3. Fee Structures: Both checking and savings accounts can have associated fees. Checking accounts might charge monthly maintenance fees, overdraft fees (for exceeding your account balance), and other transaction fees. Savings accounts might charge monthly maintenance fees or penalties for low balances or excessive withdrawals. Carefully comparing fee structures across different institutions is crucial.

4. Account Types and Variations: The market offers several variations within checking and savings accounts. Checking accounts may include interest-bearing options, business accounts, and student accounts with tailored features. Savings accounts can include money market accounts (MMAs) that offer higher interest rates but might have higher minimum balance requirements, and high-yield savings accounts that provide superior returns.

5. Security and FDIC Insurance: Most checking and savings accounts in the US are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor, per insured bank. This insurance protects your money in the event of a bank failure, offering an essential layer of security.

Exploring the Connection Between Financial Goals and Account Selection

The optimal choice between a checking and a savings account, or a combination of both, hinges entirely on individual financial goals. Someone focused on building an emergency fund will prioritize a high-yield savings account, while someone managing daily expenses will primarily rely on a checking account.

Roles and Real-World Examples: A young professional might use a checking account for payroll deposits and daily expenses, alongside a savings account for building a down payment on a house. A retired individual might rely on a checking account for regular income withdrawals and a savings account to manage healthcare expenses.

Risks and Mitigations: The primary risk associated with checking accounts is overdraft fees. Careful budgeting and monitoring account balances are crucial mitigations. With savings accounts, the risk lies in low interest rates eroding purchasing power over time. Diversifying savings into various investment vehicles mitigates this risk.

Impact and Implications: Choosing the right account significantly impacts financial well-being. Efficient account management helps individuals avoid unnecessary fees, maximize interest earnings, and facilitates achieving financial goals.

Further Analysis of Interest Rates and Account Fees

Interest rates on savings accounts fluctuate based on market conditions and the specific financial institution. High-yield savings accounts generally offer superior rates compared to standard savings accounts. However, higher rates often come with stipulations, such as minimum balance requirements.

Cause-and-Effect Relationships: Lower interest rates can hinder savings growth, while higher fees can reduce the overall value of account balances. Understanding these relationships is crucial for informed decision-making.

Impact of Fees on Savings Growth:

| Monthly Fee | Annual Fee | Interest Rate (Annual) | Impact on $1000 Deposit (After 1 Year) |

|---|---|---|---|

| $5 | $60 | 2% | $140 |

| $0 | $0 | 0.5% | $5 |

| $10 | $120 | 3% | $10 |

FAQ Section

-

What is the difference between a checking and savings account? Checking accounts are designed for daily transactions, while savings accounts are for accumulating and earning interest on savings.

-

Can I write checks from my savings account? Some banks allow limited check writing from savings accounts, but it's not a standard feature. Checking accounts provide greater check-writing capabilities.

-

What are the typical fees associated with checking and savings accounts? Fees can include monthly maintenance fees, overdraft fees (for checking), low-balance fees (for savings), and transaction fees.

-

How do I choose the right account for my needs? Consider your transaction frequency, savings goals, and fee structures. Compare different offerings from various banks and credit unions.

-

Are my funds safe in a checking or savings account? Funds in FDIC-insured accounts are protected up to $250,000 per depositor, per insured bank.

-

Can I transfer money between my checking and savings accounts? Most banks allow easy transfers between linked checking and savings accounts, often through online banking or mobile apps.

Practical Tips

-

Compare account fees and interest rates: Thoroughly research various institutions to find the most favorable terms.

-

Set up automatic transfers: Schedule regular transfers from your checking account to your savings account to build your savings consistently.

-

Monitor your account balances: Regularly review your statements to identify and address any potential issues or unusual transactions.

-

Utilize online banking tools: Take advantage of online and mobile banking for easy account management, bill payment, and transfers.

-

Consider a budget: Create a budget to effectively track income and expenses, ensuring you have sufficient funds in your checking account and steadily build your savings.

-

Explore different account types: Research various options such as high-yield savings accounts, money market accounts, and interest-bearing checking accounts.

-

Read the fine print: Carefully review the terms and conditions of any account before opening it.

-

Link your accounts: Linking your checking and savings accounts facilitates easy fund transfers and simplifies financial management.

Final Conclusion

Understanding the differences between checking and savings accounts is a fundamental aspect of responsible financial management. By choosing the right accounts and employing sound financial strategies, individuals can effectively manage their finances, achieve their savings goals, and build a strong financial foundation. The insights and practical tips provided in this article equip readers with the knowledge to make informed decisions about their banking needs, fostering financial security and prosperity. Continuously evaluate your financial goals and banking options to ensure your accounts align with your evolving needs. The journey towards financial freedom begins with informed choices and consistent effort.

Latest Posts

Latest Posts

-

How Much Does An Auto Insurance Agent Make

Apr 04, 2025

-

How Long Can My Child Stay On My Auto Insurance

Apr 04, 2025

-

Alimony Payment Definition Types Requirements

Apr 04, 2025

-

Alien Insurer Definition

Apr 04, 2025

-

What Is Embedded Derivatives

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Checking Vs Savings Account . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.