Understanding The Adjusted Gross Income

adminse

Apr 03, 2025 · 9 min read

Table of Contents

Understanding Adjusted Gross Income (AGI): A Comprehensive Guide

What makes Adjusted Gross Income (AGI) so crucial in financial planning?

AGI is the cornerstone of numerous financial decisions, influencing everything from tax liability to eligibility for government assistance programs.

Editor’s Note: Understanding Adjusted Gross Income (AGI) has been updated today.

Why Adjusted Gross Income (AGI) Matters

Adjusted Gross Income (AGI) is a crucial figure in personal finance. It's more than just a number on a tax form; it's a gateway to understanding your true financial picture and accessing various benefits and opportunities. AGI isn't simply your gross income; it's your gross income after certain deductions are applied. This seemingly small difference has significant implications for tax calculations, eligibility for government assistance programs (like healthcare subsidies), and even loan applications. Understanding AGI empowers individuals to make informed decisions regarding their finances and future planning. Its relevance extends beyond simply filing taxes; it influences healthcare costs, retirement planning, and even eligibility for certain scholarships. For businesses, understanding AGI can help in accurate payroll processing and compliance with tax regulations. In short, mastering AGI is key to effective financial management.

Overview of the Article

This article delves into the intricacies of AGI, exploring its definition, calculation, and practical applications. We'll examine the various deductions that impact AGI, discussing their eligibility criteria and limitations. Readers will gain a comprehensive understanding of how AGI affects tax liability, access to government programs, and other financial decisions. The article is supported by extensive research, incorporating relevant tax laws and regulations to ensure accuracy and provide practical, actionable insights. By the end, readers will be equipped to confidently calculate their AGI and leverage this knowledge for informed financial planning.

Research and Effort Behind the Insights

This article draws upon extensive research from the Internal Revenue Service (IRS) publications, relevant tax codes, and financial planning resources. The information presented is meticulously reviewed to ensure accuracy and compliance with current tax laws. The goal is to provide readers with clear, concise, and up-to-date information that can be readily applied to their personal financial situations.

Key Takeaways: Understanding Your AGI

| Key Point | Description |

|---|---|

| Definition of AGI | Gross income minus certain "above-the-line" deductions. |

| Impact on Tax Liability | Determines your eligibility for certain tax deductions and credits, significantly influencing your tax burden. |

| Eligibility for Programs | Influences qualification for various government assistance programs, including healthcare subsidies and student loan forgiveness. |

| Financial Planning Tool | Essential for retirement planning, estate planning, and other long-term financial strategies. |

| Calculating Your AGI | Requires understanding which deductions are applicable to your specific circumstances. |

| Importance of Accuracy | Incorrect AGI calculation can lead to penalties and complications with tax authorities. |

Smooth Transition to Core Discussion

Let's now delve deeper into the core components of AGI, starting with its precise definition and the key deductions that contribute to its calculation.

Exploring the Key Aspects of Adjusted Gross Income

-

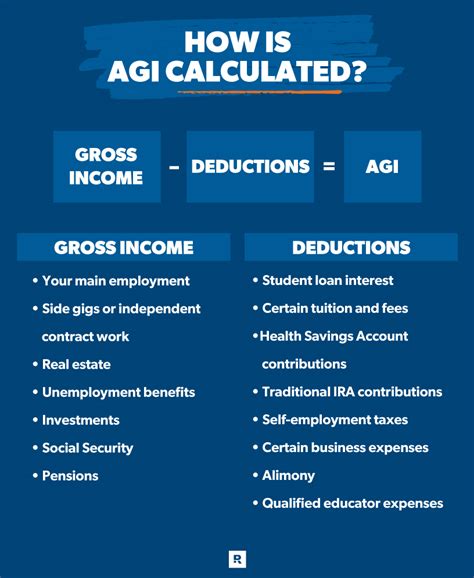

Definition and Calculation: AGI is calculated by subtracting certain allowable deductions (called "above-the-line" deductions) from your gross income. Gross income encompasses all sources of income, including wages, salaries, self-employment income, interest, dividends, capital gains, and rental income. The key difference between AGI and gross income lies in these above-the-line deductions.

-

Above-the-Line Deductions: These are deductions subtracted directly from gross income to arrive at AGI. Unlike itemized deductions (discussed later), above-the-line deductions are universally available, regardless of whether you itemize or take the standard deduction. Common above-the-line deductions include:

- IRA Deductions: Contributions to traditional Individual Retirement Accounts (IRAs) can be deducted, subject to income limitations.

- Self-Employment Tax Deduction: The self-employed can deduct one-half of their self-employment tax.

- Health Savings Account (HSA) Deduction: Contributions to an HSA are deductible, provided you have a qualified high-deductible health plan.

- Student Loan Interest Deduction: A deduction for student loan interest payments is available, up to a certain limit.

- Educator Expenses: Certain unreimbursed educator expenses may be deductible.

- Alimony Payments (for divorces finalized before 2019): Alimony paid under certain conditions is deductible. Note that this deduction is no longer available for divorces finalized in 2019 or later.

-

AGI and Tax Brackets: Your AGI determines which tax bracket you fall into. Tax brackets are ranges of income subject to specific tax rates. A higher AGI generally means a higher tax rate, though the actual tax owed is also influenced by other factors, including deductions and credits.

-

AGI and Tax Credits: Many tax credits are based on or limited by AGI. For example, the earned income tax credit (EITC) and the child tax credit have income limits based on AGI. Knowing your AGI is essential for determining eligibility for these valuable tax breaks.

-

AGI and Government Programs: Numerous government programs use AGI as a criterion for determining eligibility. This includes programs related to healthcare, education, and housing assistance. Understanding your AGI is crucial for determining whether you qualify for these important programs.

-

AGI and Financial Planning: AGI is a fundamental component in various financial planning strategies. It plays a role in retirement planning, estate planning, and even loan applications. A well-defined understanding of AGI helps in making informed financial decisions.

Closing Insights

Understanding AGI is not merely a matter of tax compliance; it's a critical aspect of effective financial management. By accurately calculating your AGI and understanding its implications, individuals can optimize their tax burden, access valuable government programs, and make informed decisions about their financial future. From retirement planning to healthcare decisions, the impact of AGI is far-reaching and significant. The information discussed above provides a solid foundation for navigating the complexities of AGI and leveraging its importance to personal financial well-being. Mastering AGI is a crucial step towards achieving long-term financial success.

Exploring the Connection Between Tax Credits and AGI

Tax credits directly reduce your tax liability, dollar-for-dollar. Many tax credits, however, have income limitations based on AGI. This means that even if you qualify for a particular credit, the amount you receive may be reduced or eliminated if your AGI exceeds a specific threshold. For instance, the Earned Income Tax Credit (EITC) is designed to help low-to-moderate-income working individuals and families, and its maximum benefit is phased out as AGI increases. Similarly, the Child Tax Credit has income limits based on AGI. Understanding these AGI limitations is crucial for accurately calculating your tax liability and maximizing your tax benefits. Failing to account for these limitations can lead to an inaccurate calculation of your refund or tax owed.

Further Analysis of Above-the-Line Deductions

| Deduction | Description | AGI Impact |

|---|---|---|

| IRA Deductions | Contributions to traditional IRAs are deductible, subject to income limitations. | Reduces AGI, potentially lowering tax liability |

| Self-Employment Tax Deduction | Self-employed individuals can deduct one-half of their self-employment tax. | Reduces AGI, lowering taxable income |

| HSA Deductions | Contributions to a Health Savings Account (HSA) are deductible, provided you have a qualified high-deductible health plan. | Reduces AGI, potentially lowering tax liability |

| Student Loan Interest Deduction | A deduction is available for student loan interest payments, up to a certain limit. | Reduces AGI, potentially lowering tax liability |

| Educator Expenses | Certain unreimbursed educator expenses (up to a limit) may be deductible. | Reduces AGI, potentially lowering tax liability |

FAQ Section

-

Q: What is the difference between gross income and AGI? A: Gross income is your total income from all sources. AGI is your gross income minus certain above-the-line deductions.

-

Q: Why is AGI important for tax purposes? A: Your AGI determines your eligibility for various tax deductions and credits, impacting your tax liability.

-

Q: How do I calculate my AGI? A: You calculate your AGI by subtracting allowable above-the-line deductions from your gross income. Form 1040 provides the necessary lines for this calculation.

-

Q: Does AGI affect my eligibility for government assistance programs? A: Yes, many government programs, such as healthcare subsidies and student loan forgiveness, use AGI to determine eligibility.

-

Q: What happens if I incorrectly calculate my AGI? A: An incorrect calculation can lead to penalties and complications with the IRS.

-

Q: Where can I find more information about AGI and its implications? A: The IRS website (irs.gov) and publications from reputable financial institutions provide comprehensive information.

Practical Tips

-

Gather all income documentation: Collect W-2s, 1099s, and other relevant documents to accurately determine your gross income.

-

Identify applicable above-the-line deductions: Review the IRS guidelines to identify deductions you qualify for, such as IRA contributions, self-employment tax, or student loan interest.

-

Maintain accurate records: Keep meticulous records of all income and expenses to support your AGI calculation.

-

Use tax software or consult a professional: Tax software can simplify the AGI calculation process. If needed, consult a tax professional for assistance.

-

Understand AGI limitations for tax credits: Be aware of how AGI limits the amount of certain tax credits you can claim.

-

Review your AGI annually: Your financial situation may change annually, impacting your AGI. Review your AGI calculations each year to ensure accuracy.

-

Plan for future AGI changes: Consider how future income changes, such as promotions or job changes, will influence your AGI and tax obligations.

-

Utilize AGI information for financial planning: Use your AGI to make informed decisions about retirement savings, investment strategies, and other long-term financial goals.

Final Conclusion

Adjusted Gross Income (AGI) is a fundamental concept in personal finance with far-reaching implications. From tax liability to eligibility for government programs, understanding and accurately calculating your AGI is paramount. By following the guidance provided in this article and staying informed about relevant tax laws and regulations, individuals can effectively manage their finances and leverage AGI to their advantage. Remember, accurate AGI calculation is essential for both tax compliance and informed financial decision-making. Continue to research and stay updated on changes to tax laws to ensure you are always maximizing your financial well-being.

Latest Posts

Latest Posts

-

All Cash All Stock Offer Definition Downsides Alternatives

Apr 04, 2025

-

How To Cancel Geico Auto Insurance

Apr 04, 2025

-

How Much Does An Auto Insurance Agent Make

Apr 04, 2025

-

How Long Can My Child Stay On My Auto Insurance

Apr 04, 2025

-

Alimony Payment Definition Types Requirements

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Understanding The Adjusted Gross Income . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.