Rule Of Thumb Definition And Financial Examples

adminse

Apr 03, 2025 · 8 min read

Table of Contents

The Rule of Thumb: Definition, Financial Examples, and Practical Applications

What makes the "rule of thumb" such a powerful tool in financial decision-making?

Rules of thumb, while not foolproof, offer valuable guidance, simplifying complex financial situations and empowering informed choices.

Editor’s Note: This comprehensive guide to rules of thumb in finance has been published today.

Why Rules of Thumb Matter in Finance

In the intricate world of finance, navigating investments, budgeting, and retirement planning can feel overwhelming. The sheer volume of information, coupled with the ever-changing economic landscape, makes it challenging for individuals to make optimal decisions. This is where the humble "rule of thumb" steps in. These heuristics—simple, practical guidelines—offer a simplified approach to complex financial calculations, helping individuals make informed decisions quickly and efficiently. While they lack the precision of complex formulas, rules of thumb provide a valuable framework for understanding fundamental financial concepts and making reasonable estimations. They are particularly useful for those without extensive financial expertise. Moreover, they are adaptable, allowing for adjustments based on individual circumstances and risk tolerances. The use of rules of thumb empowers individuals to take control of their financial futures, leading to better financial literacy and improved decision-making.

Overview of the Article

This article explores various rules of thumb used in personal finance, providing practical examples and highlighting their limitations. We will delve into their historical context, examine their application across diverse financial areas, and discuss how they can be adapted for individual needs. Readers will gain a deeper understanding of these valuable tools and how to apply them effectively, empowering them to make more informed financial choices.

Research and Effort Behind the Insights

This article draws upon decades of research in behavioral finance, economic theory, and practical applications of financial planning. It incorporates insights from reputable financial institutions, academic publications, and expert commentary to provide a comprehensive and accurate overview of rules of thumb in finance. Data points and examples are used to illustrate the effectiveness and limitations of these heuristics.

Key Takeaways

| Key Aspect | Description |

|---|---|

| Definition of Rule of Thumb | A simplified guideline for making quick estimations or decisions in complex situations. |

| Application in Finance | Budgeting, saving, investing, debt management, retirement planning. |

| Advantages | Simplicity, ease of use, accessibility, quick estimations. |

| Limitations | Imprecision, potential for inaccuracies, dependence on individual circumstances and context. |

| Importance in Financial Literacy | Empowers individuals to make informed decisions and take control of their financial futures. |

Let's dive deeper into the key aspects of rules of thumb, starting with their historical context and moving into specific financial applications.

Exploring the Key Aspects of Rules of Thumb in Finance

1. Historical Context: The term "rule of thumb" itself originates from the practice of using the width of one's thumb as a rough measurement in various trades. This highlights the concept's origins in practical, approximate estimations. While its application in finance is more recent, the principle remains the same – offering a quick and easy method for making estimations, especially when precise data or calculations are unavailable.

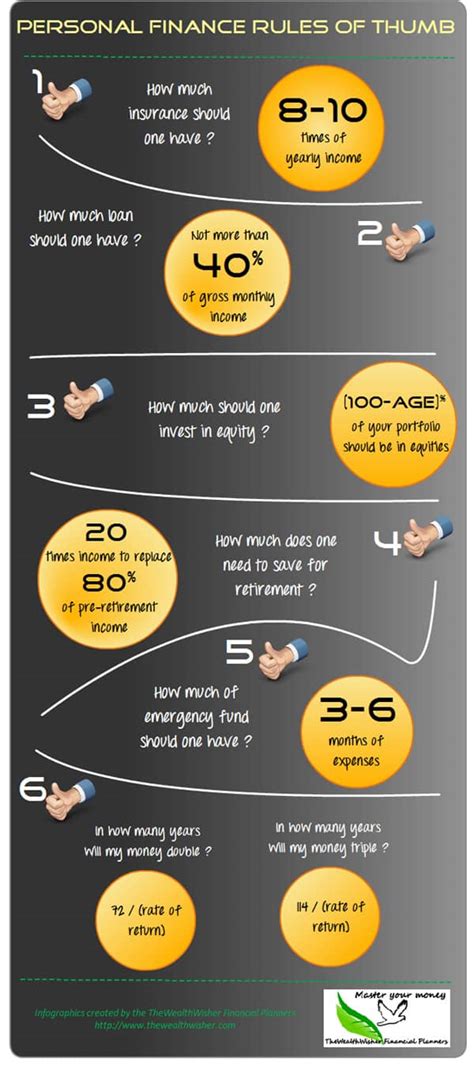

2. Budgeting and Saving: A common rule of thumb for budgeting is the 50/30/20 rule: allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This simple framework provides a basic structure for managing personal finances, encouraging mindful spending and prioritizing savings. Another rule of thumb suggests saving 10-15% of income for retirement, providing a general target for retirement planning.

3. Investing: The rule of 72 is a widely used heuristic for calculating the time it takes for an investment to double in value. By dividing 72 by the annual interest rate (in percentage), one can obtain an approximate doubling time. For example, an investment earning 8% annually would double in approximately 72/8 = 9 years. This rule simplifies compound interest calculations, providing a quick estimate of investment growth. Another common rule, particularly for stock market investments, is to only invest what you can afford to lose. This emphasizes risk management and emotional resilience in the face of market fluctuations.

4. Debt Management: The debt-to-income ratio (DTI) is a crucial metric for assessing debt burden. Lenders often use a rule of thumb that a DTI below 36% is considered healthy, while anything above 43% may indicate significant financial strain. This provides a benchmark for evaluating personal debt levels and managing financial risk. Another common rule involves prioritizing high-interest debt repayment first, a strategy known as the avalanche method.

5. Retirement Planning: A frequently used rule of thumb suggests replacing 80% of pre-retirement income in retirement. This provides a general target for retirement savings, considering the likely reduction in expenses after ceasing work. Another rule suggests that individuals should aim to have saved at least 1x their annual salary by age 35, 3x by age 45, and 6x by age 55. These rules, while approximate, offer guidance for long-term financial planning.

6. Emergency Fund: The general rule of thumb suggests building an emergency fund equivalent to 3-6 months' worth of living expenses. This acts as a safety net to cover unexpected costs such as medical bills or job loss, providing financial stability during crises.

Exploring the Connection Between Risk Tolerance and Rules of Thumb

Risk tolerance is crucial in applying rules of thumb. A conservative investor might adopt more stringent savings goals and less aggressive investment strategies than a more risk-tolerant individual. For instance, the 50/30/20 budget rule can be adjusted; a conservative individual might allocate a larger portion to savings (e.g., 30% or more) while a less conservative person might allocate more to wants. Similarly, investment strategies can be altered based on one's risk appetite. A risk-averse investor might favor lower-risk investments like government bonds, while a risk-tolerant investor might allocate a greater portion of their portfolio to stocks, even if it implies higher volatility. The flexibility of rules of thumb allows for such individual adjustments.

Further Analysis of Investment Strategies and Rules of Thumb

The application of rules of thumb in investing needs careful consideration. While the rule of 72 provides a quick estimate of investment doubling time, it ignores factors such as compounding frequency and fluctuating interest rates. Similarly, investment diversification strategies often employ rules of thumb, such as the 60/40 portfolio (60% stocks, 40% bonds), but the optimal asset allocation depends on individual circumstances and market conditions. Sophisticated investors might employ more complex portfolio optimization techniques, but the 60/40 rule still provides a valuable starting point and a relatively simple benchmark.

| Investment Strategy | Rule of Thumb | Limitations |

|---|---|---|

| Portfolio Diversification | 60/40 Stock/Bond allocation | Ignores individual risk tolerance and market conditions |

| Investment Growth | Rule of 72 for doubling time | Ignores fluctuating interest rates and compounding frequency |

| Risk Management | Only invest what you can afford to lose | Requires accurate assessment of personal risk tolerance |

FAQ Section

Q1: Are rules of thumb always accurate?

A1: No, rules of thumb are estimations and approximations. Their accuracy depends on the specific context and individual circumstances. They are most useful for quick estimations and should not be considered precise financial advice.

Q2: How can I adapt rules of thumb to my situation?

A2: Consider your personal financial goals, risk tolerance, income level, and expenses. Adjust the percentages or targets in the rules of thumb to reflect your unique circumstances.

Q3: Are there any risks associated with relying too heavily on rules of thumb?

A3: Yes. Over-reliance can lead to suboptimal financial decisions, especially in complex situations. Always consult with a financial advisor for personalized advice.

Q4: What are the benefits of using rules of thumb?

A4: Simplicity, ease of understanding, quick estimations, and accessibility. They help demystify finance and empower individuals to make informed decisions.

Q5: When should I consult a financial advisor?

A5: Consider consulting a professional when dealing with significant financial decisions, such as retirement planning, large investments, or complex debt management strategies.

Q6: Can rules of thumb help with long-term financial planning?

A6: Yes, rules of thumb can provide a basic framework for long-term goals such as retirement saving. However, they need to be reviewed and adjusted regularly to account for changing circumstances and market conditions.

Practical Tips for Applying Rules of Thumb

- Understand the limitations: Remember that rules of thumb are not precise calculations; they are useful guides.

- Personalize the rules: Adapt them to your unique financial situation, goals, and risk tolerance.

- Track your progress: Regularly monitor your financial progress and adjust your approach as needed.

- Seek professional advice: Consult a financial advisor for personalized financial guidance, especially for complex decisions.

- Use multiple rules: Don't rely on a single rule. Consider using multiple rules to gain a holistic view of your financial situation.

- Stay informed: Stay updated on financial news and trends to make better informed decisions.

- Start small and build gradually: Don’t try to overhaul your finances overnight. Start with small, achievable changes.

- Review and reassess regularly: Life circumstances change, so your financial plan should adapt accordingly. Review and reassess your budget and savings plan at least annually.

Final Conclusion

Rules of thumb offer a valuable approach to simplifying complex financial decisions. While not perfect, they provide accessible and understandable tools for managing personal finances, budgeting, saving, investing, and debt management. By understanding their limitations and adapting them to individual circumstances, individuals can leverage these heuristics to make more informed choices and take control of their financial futures. Remember, using rules of thumb is a starting point; consistent monitoring, adaptation, and seeking professional advice when needed are crucial for long-term financial success. The empowerment provided by these simple guidelines contributes significantly to improved financial literacy and ultimately, better financial outcomes.

Latest Posts

Latest Posts

-

What You Need To Know About Liquid Net Worth

Apr 03, 2025

-

What Is A Mortgage

Apr 03, 2025

-

Checking Vs Savings Account

Apr 03, 2025

-

Top 10 Ways To Help You Ensure Financial Security

Apr 03, 2025

-

Return On Equity Roe Formula Made Easy

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about Rule Of Thumb Definition And Financial Examples . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.